Introduction: Setting financial goals is critical to achieving financial independence and security. Without clear and actionable goals, it's easy to lose track of your finances and fall short of long-term wealth. In this blog, we'll explore who should set financial goals, how to set realistic ones and share examples to help guide you in your personal financial journey.

Why Setting Financial Goals is Crucial

Financial goals give you direction and purpose. They act as a roadmap for your financial future, helping you manage your spending, save for future expenses, and invest for wealth growth. Whether you're aiming to save for an emergency fund, plan for a big purchase, or secure a comfortable retirement, financial goals help ensure you're on the right track.

Example: Imagine trying to save ₹50,000 in one year without a concrete plan. You’ll likely struggle to get there. Now, if you break it down and set a goal to save ₹4,200 per month, it becomes far more achievable and easier to track.

Who Should Set Financial Goals?

Everyone should set financial goals, regardless of age, income, or financial situation. Here are some profiles:

- Students: Planning to save for education or side hustles.

- Young Professionals: Setting short-term goals like creating an emergency fund or saving for a down payment on a house.

- Families: Managing household budgets, saving for kids' education, and long-term investments.

- Retirees: Ensuring retirement funds are adequate for future needs.

Example: A young professional earning ₹50,000 per month should set aside 20% for long-term savings and investments while focusing on building an emergency fund.

How to Set Realistic Financial Goals

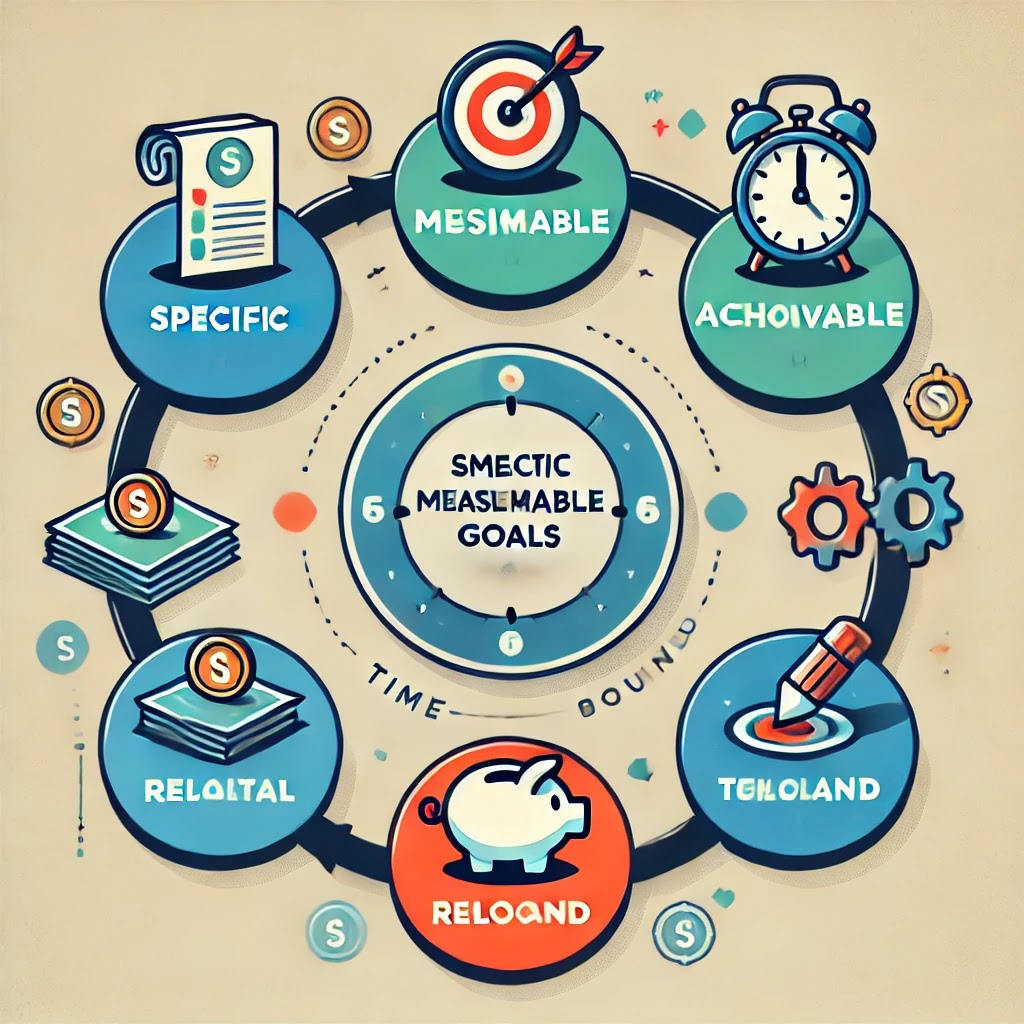

Setting vague or overly ambitious financial goals can lead to frustration. The best method to ensure success is using the SMART goal framework—goals should be Specific, Measurable, Achievable, Relevant, and Time-bound.

1. Specific

Define exactly what you want to achieve.

- Example: "Save ₹1,00,000 for an emergency fund" is more specific than "Save money."

2. Measurable

Ensure your goal can be tracked with numbers or milestones.

- Example: "Save ₹5,000 each month" allows you to track progress toward your ₹1,00,000 goal.

3. Achievable

Set realistic goals based on your financial situation.

- Example: If you can only afford to save ₹2,500 per month, adjust your timeline or goals.

4. Relevant

Align your goals with your financial priorities.

- Example: If your priority is financial security, focus on an emergency fund before investing heavily in the stock market.

5. Time-bound

Set a deadline for your goals to motivate you to stay on track.

- Example: "Save ₹1,00,000 within 12 months."

Breaking Down Financial Goals: Short-Term, Medium-Term, and Long-Term

1. Short-Term Goals (0-2 years)

These are smaller, more immediate goals you can accomplish within a short period.

- Example: Building an emergency fund of ₹1,00,000 within 1 year.

2. Medium-Term Goals (2-5 years)

These are for milestones within the next few years.

- Example: Saving for a car or home down payment.

3. Long-Term Goals (5+ years)

These are larger financial objectives that require a long-term commitment.

- Example: Saving ₹25,00,000 for retirement over 20 years.

Example Use Case: A Step-by-Step SMART Goal for a Young Professional

- Specific: Save ₹5,00,000 for a home down payment.

- Measurable: Save ₹15,000 per month.

- Achievable: Reduce unnecessary expenses and invest in a high-yield savings account.

- Relevant: The goal aligns with the individual’s desire to buy a home within the next 5 years.

- Time-bound: Reach the goal in 3 years.

How to Stay on Track with Financial Goals

- Automate Your Savings: Set up automatic transfers to your savings account to ensure you’re consistently saving.

- Track Your Progress: Regularly check how close you are to reaching your goal.

- Reassess and Adjust: Life changes, and so should your goals. Adjust your financial goals accordingly if you experience a change in income or priorities.

Conclusion: Achieving Financial Success with Clear Goals

Setting realistic and well-defined financial goals is the cornerstone of economic success. With a clear direction and the SMART framework, anyone can take control of their financial future. Whether you're a student just starting out, a young professional managing new income, or a retiree ensuring your funds last, setting goals is the key to staying financially secure.

Ready to take the next step in your financial journey? Subscribe for more tips on budgeting, saving, and investing! And don't miss Day 3, where we’ll discuss creating and sticking to a monthly budget with practical tips and templates.

No comments:

Post a Comment